VQ-TR: Vector Quantized Attention for Time Series Forecasting

{kind=link}

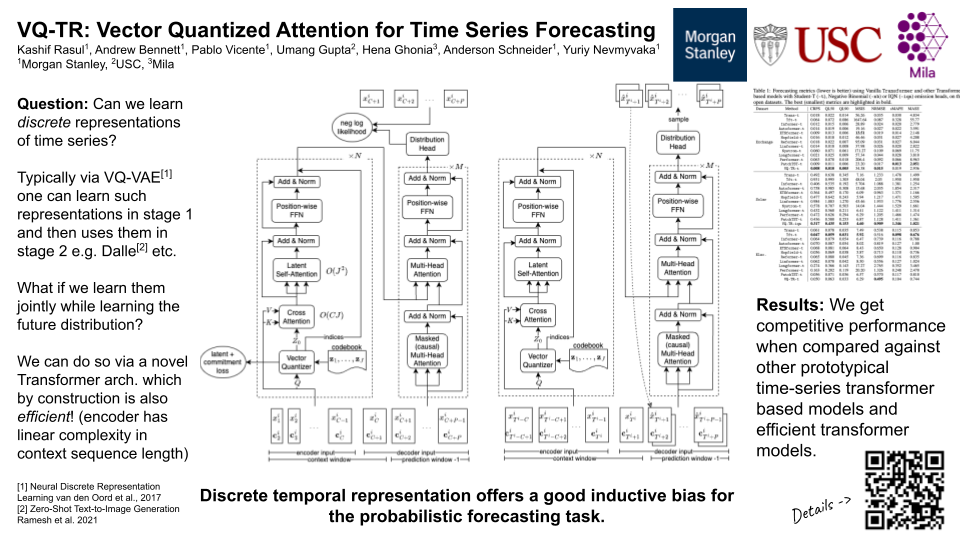

Abstract

Probabilistic time series forecasting is a challenging problem due to the long sequences involved, the large number of samples needed for accurate probabilistic inference, and the need for real-time inference in many applications. These challenges necessitate methods that are not only accurate but computationally efficient. Unfortunately, most current state-of-the-art methods for time series forecasting are based on Transformers, which scale poorly due to quadratic complexity in sequence length, and are therefore needlessly computationally inefficient. Moreover, with a few exceptions, these methods have only been evaluated for non-probabilistic point estimation. In this work, we address these two shortcomings.For the first, we introduce VQ-TR, which maps large sequences to a discrete set of latent representations as part of the Attention module. This not only allows us to attend over larger context windows with linear complexity in sequence length but also allows for effective regularization to avoid overfitting.For the second, we provide what is to the best of our knowledge the first systematic comparison of modern Transformer-based time series forecasting methods for probabilistic forecasting. In this comparison, we find that VQ-TR performs better or comparably to all other methods while being computationally efficient.