SynQubi: A Quantum-Optimized Multi-Agent For Risk-Aware Financial Decision-Making

{kind=link}

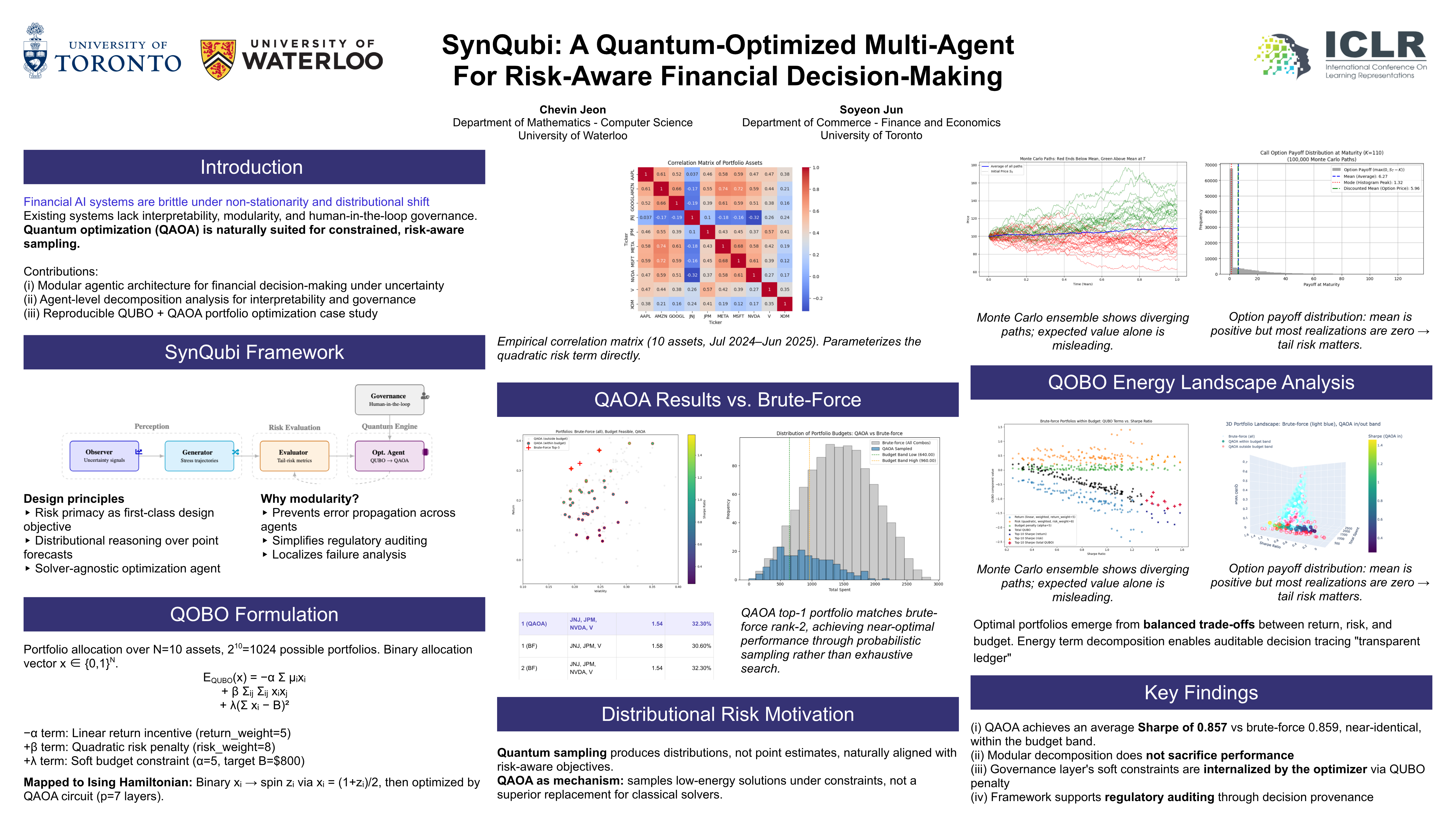

Abstract

Financial decision-making systems increasingly operate under non-stationarity, uncertainty, and high-stakes risk, where brittle or opaque optimization pipelines can lead to severe failures. Although recent advances in Financial AI and agentic architectures enable more adaptive decision-making, integrating powerful optimization methods in a manner that is safe, interpretable, and governable remains an open challenge. We propose a modular agentic framework for risk-aware financial decision-making that decomposes perception, scenario generation, risk evaluation, optimization, and oversight into interacting agents. Rather than prioritizing return maximization alone, the framework emphasizes robustness, interpretability, and human-in-the-loop control. We illustrate the framework through a reproducible portfolio allocation case study formulated as a quadratic unconstrained binary optimization (QUBO) problem, where binary decision variables encode asset selection and the objective jointly captures expected return, risk, and budget constraints. The resulting QUBO is optimized using the Quantum Approximate Optimization Algorithm (QAOA). By benchmarking QAOA-generated portfolios against exhaustive brute-force enumeration, we show how probabilistic, constraint-aware optimization can function as a risk-aware proposal mechanism within an agentic pipeline, rather than as an autonomous decision authority.