PMDformer: Patch-Mean Decoupling Information Transformer for Long-term Forecasting

{kind=link}

Abstract

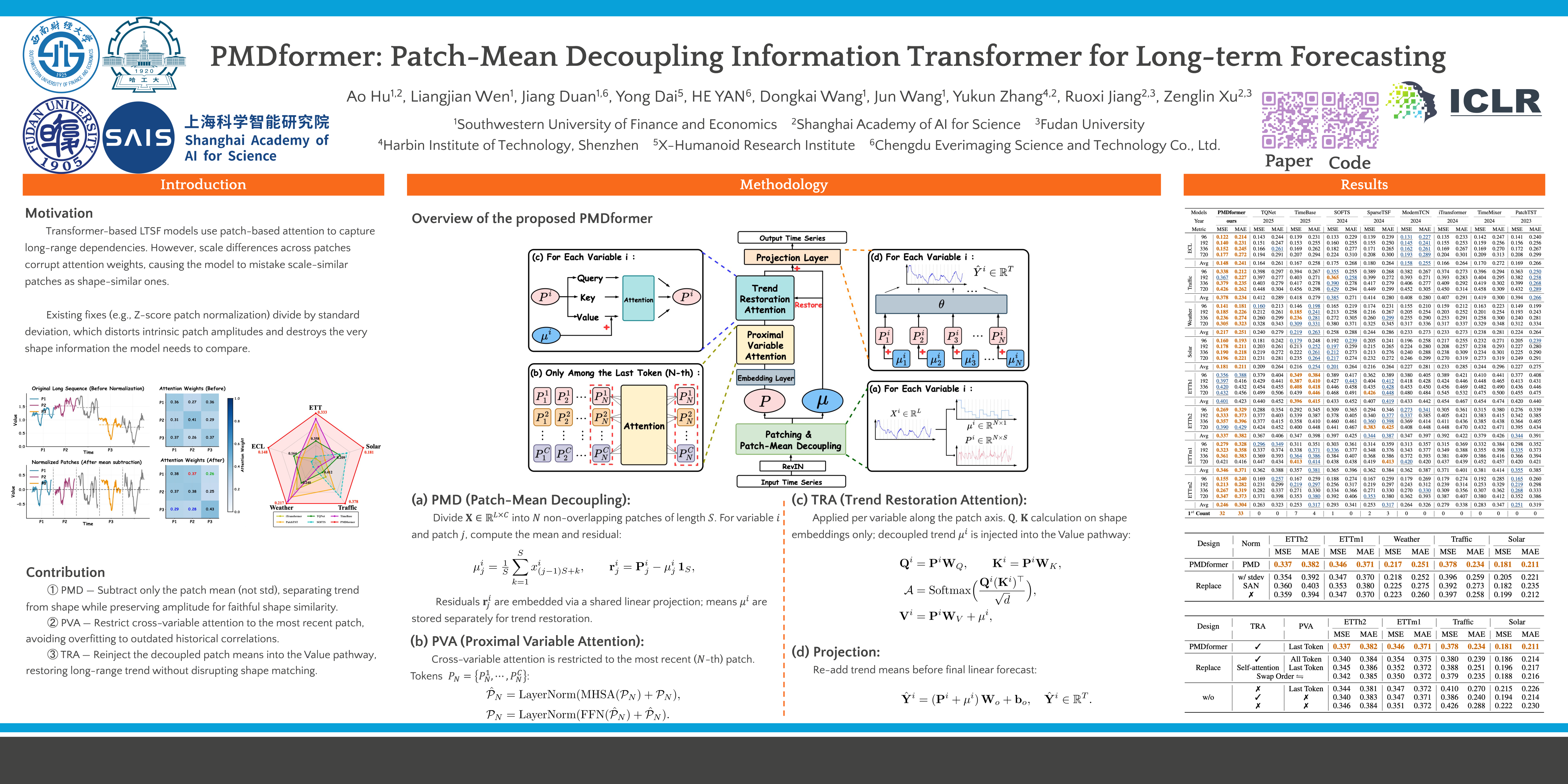

Long-term time series forecasting (LTSF) plays a crucial role in fields such as energy management, finance, and traffic prediction. Transformer-based models have adopted patch-based strategies to capture long-range dependencies, but accurately modeling shape similarities across patches and variables remains challenging due to scale differences. To address this, we introduce patch-mean decoupling (PMD), which separates the trend and residual shape information by subtracting the mean of each patch, preserving the original structure and ensuring that the attention mechanism captures true shape similarities. Futhermore, to more effectively model long-range dependencies and capture cross-variable relationships, we propose Trend Restoration Attention (TRA) and Proximal Variable Attention (PVA). The former module reintegrates the decoupled trend from PMD while calculating attention output. And the latter focuses cross-variable attention on the most relevant, recent time segments to avoid overfitting on outdated correlations. Combining these components, we propose PMDformer, a model designed to effectively capture shape similarity in long-term forecasting scenarios. Extensive experiments indicate that PMDformer outperforms existing state-of-the-art methods in stability and accuracy across multiple LTSF benchmarks. The code is available at https://github.com/aohu1105/PMDformer.