Data-driven mean-variability optimization of PV portfolios with automatic differentiation

{kind=link}

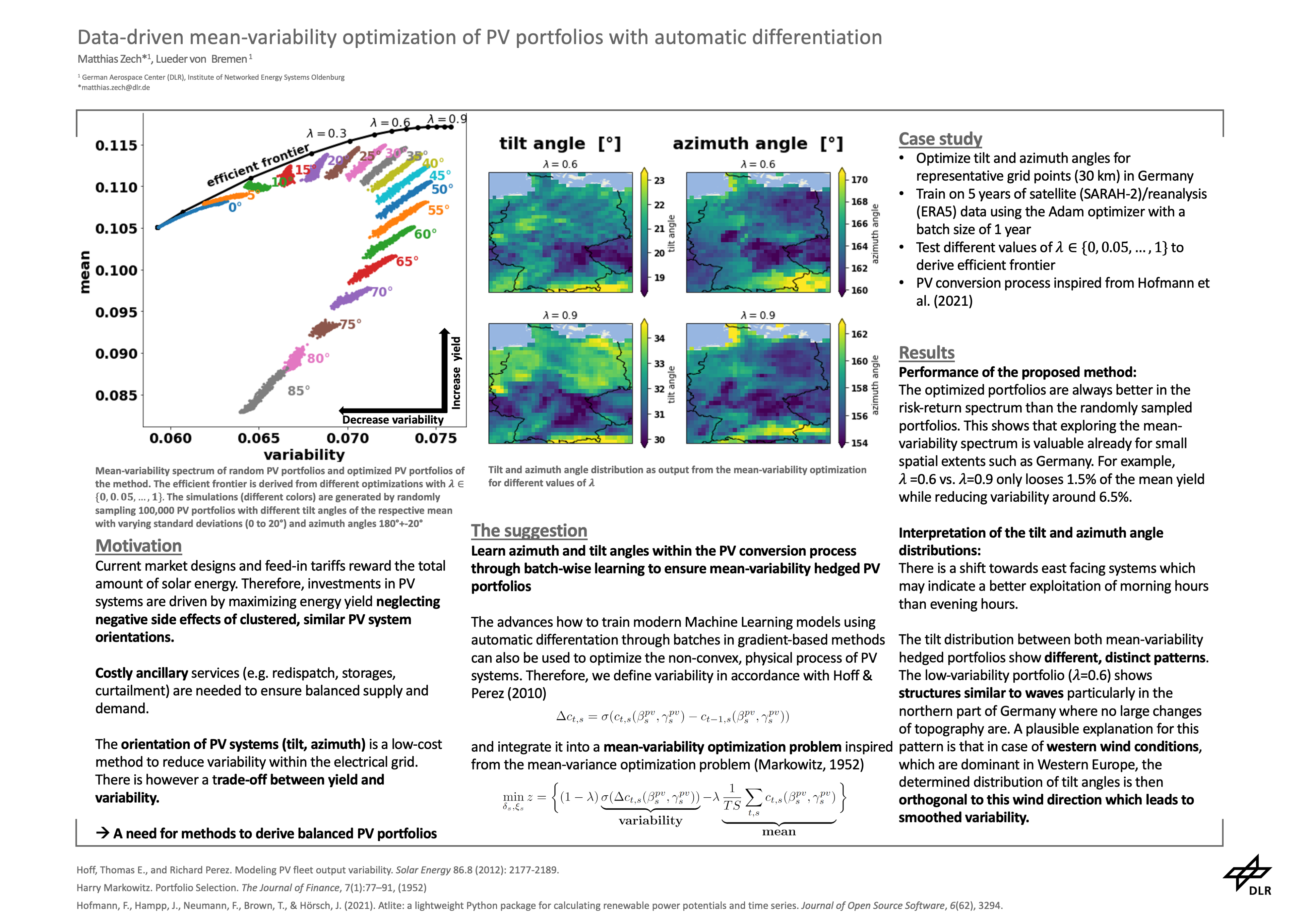

Abstract

The large-scale deployment of renewable energy is the key pillar to achieve carbon-neutral energy systems and as part of this transition, PV has a crucial role as an affordable, clean energy. To promote PV expansion, policy designs have been developed which rely on yield maximization to increase the total PV energy supply in energy systems. Focusing on yield maximization, however, ignores negative side-effects such as an increased variability due to similar-orientated PV systems at clustered regions. This paper introduces a data-driven method based on the well-studied findings from modern portfolio theory to derive mean-variability balanced PV portfolios with smartly orientated tilt and azimuth angles. The formulated non-convex optimization problem is solved based on automatically differentiating the physical PV conversion model subject to individual tilt and azimuth angles of representative grid points. To illustrate the performance of the proposed method, a case study is designed to derive efficient frontiers in the mean-variability spectrum of Germany's PV portfolio. The proposed method allows decision-makers to hedge between uncertainty and yield of PV portfolios making it attractive as a tool for policy design. This is the first study highlighting the problem of ignoring the uncertainty within yield maximization policy schemes and introduces a method how to tackle this issue using modern methods inspired by Machine Learning.