Generalized Principal-Agent Problem with a Learning Agent

Tao Lin ⋅ Yiling Chen

2025 Poster

{kind=link}

Abstract

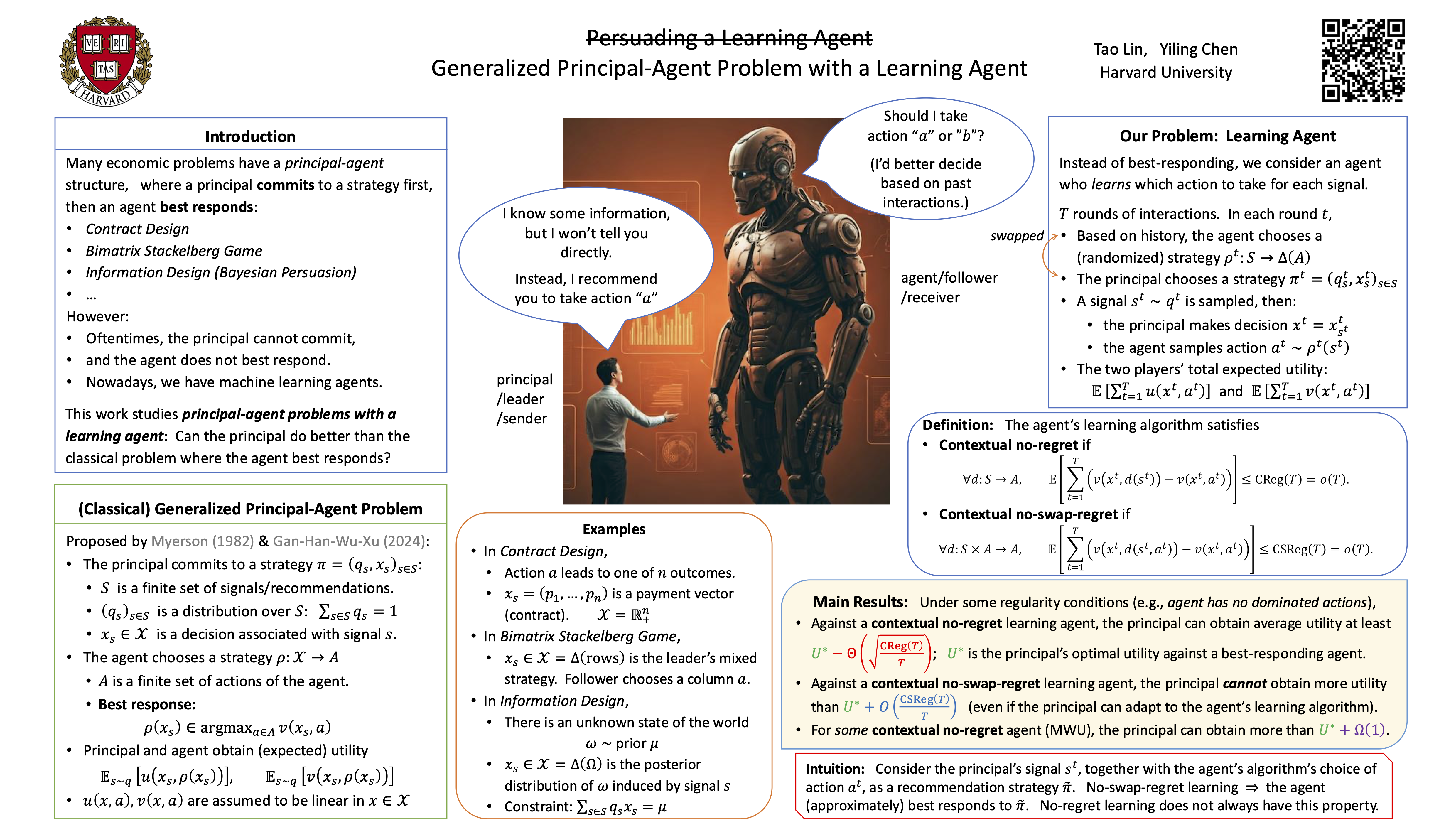

Generalized principal-agent problems, including Stackelberg games, contract design, and Bayesian persuasion, are a class of economic problems where an agent best responds to a principal's committed strategy. We study repeated generalized principal-agent problems under the assumption that the principal does not have commitment power and the agent uses algorithms to learn to respond to the principal. We reduce this problem to a one-shot generalized principal-agent problem where the agent approximately best responds. Using this reduction, we show that: (1) if the agent uses contextual no-regret learning algorithms with regret $\mathrm{Reg}(T)$, then the principal can guarantee utility at least $U^* - \Theta\big(\sqrt{\tfrac{\mathrm{Reg}(T)}{T}}\big)$, where $U^*$ is the principal's optimal utility in the classic model with a best-responding agent.(2) If the agent uses contextual no-swap-regret learning algorithms with swap-regret $\mathrm{SReg}(T)$, then the principal cannot obtain utility more than $U^* + O(\frac{\mathrm{SReg(T)}}{T})$. But (3) if the agent uses mean-based learning algorithms (which can be no-regret but not no-swap-regret), then the principal can sometimes do significantly better than $U^*$.These results not only refine previous results in Stackelberg games and contract design, but also lead to new results for Bayesian persuasion with a learning agent and all generalized principal-agent problems where the agent does not have private information.

Video

Chat is not available.

Successful Page Load