KooNPro: A Variance-Aware Koopman Probabilistic Model Enhanced by Neural Process for Time Series Forecasting

{kind=link}

Abstract

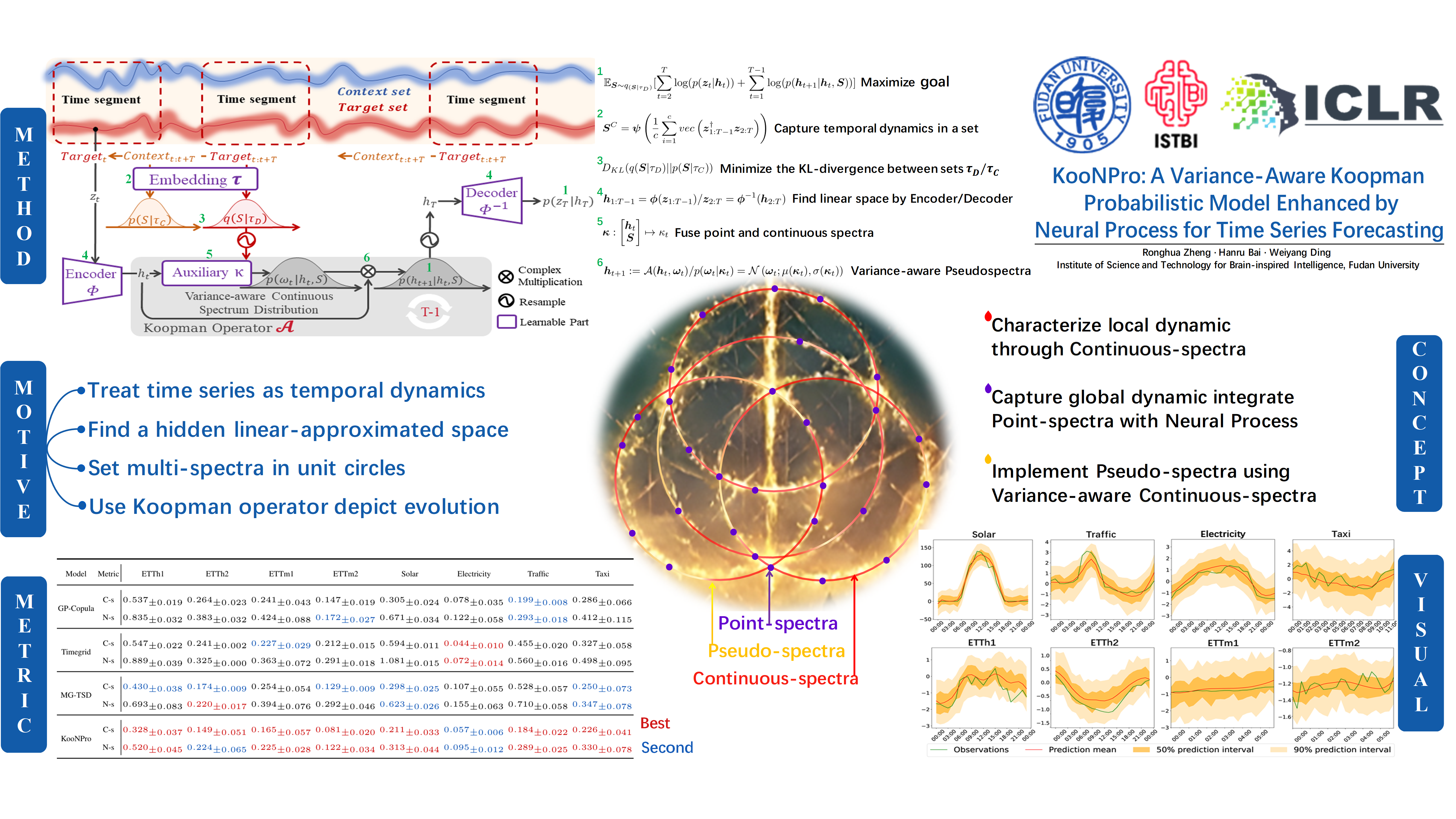

The probabilistic forecasting of time series is a well-recognized challenge, particularly in disentangling correlations among interacting time series and addressing the complexities of distribution modeling. By treating time series as temporal dynamics, we introduce KooNPro, a novel probabilistic time series forecasting model that combines variance-aware deep Koopman model with Neural Process. KooNPro introduces a variance-aware continuous spectrum using Gaussian distributions to capture complex temporal dynamics with improved stability. It further integrates the Neural Process to capture fine dynamics, enabling enhanced dynamics capture and prediction. Extensive experiments on nine real-world datasets demonstrate that KooNPro consistently outperforms state-of-the-art baselines. Ablation studies highlight the importance of the Neural Process component and explore the impact of key hyperparameters. Overall, KooNPro presents a promising novel approach for probabilistic time series forecasting.